Is a Living Trust the Key to Smooth Inheritance Planning? Here’s What You Need to Know.

(Disclaimer: This article is for informational purposes only and should not be considered legal advice. Please consult an attorney for guidance on your specific situation.)

Building wealth throughout your life allows you to create a secure future for yourself and your loved ones. But have you considered the most effective way to pass on your legacy? A living trust might be the answer you’ve been searching for.

What is a Living Trust?

Think of a living trust as a legal document that acts as a container for your assets. You, the grantor, can transfer ownership of various assets – like your house, investments, or even a treasured family heirloom – into the trust while you’re still alive and well. Here’s the beauty: you remain in control! You can manage and benefit from these assets just as you always have.

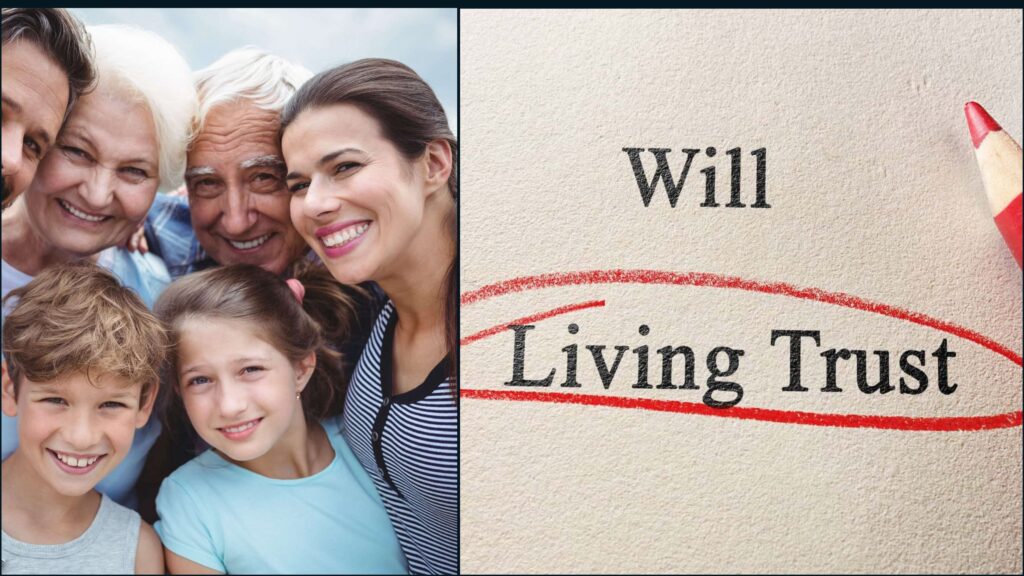

Living Trust vs. Will: What’s the Difference?

Both living trusts and wills aim to manage your assets after you’re gone. However, they differ in how efficiently they achieve this goal. A will comes into play only after your passing. It can be a lengthy and public process called probate, where a court oversees distributing your assets according to your wishes. This can be time-consuming, expensive, and can even expose the details of your estate to the public eye.

Benefits of a Living Trust

Bypassing Probate: A living trust allows your designated beneficiaries to receive your assets directly, avoiding the probate process altogether. This saves your loved ones time, money, and unnecessary stress during a difficult time.

Enhanced Privacy: Unlike wills exposed in probate court, living trusts remain private documents. This ensures your financial wishes and asset distribution remain confidential.

Maintaining Control: The power remains in your hands. You can manage and benefit from the assets held within the trust throughout your lifetime. And, should your circumstances change, you have the flexibility to modify the terms of the trust at any point.

Successor Trustee: If you become incapacitated due to illness or age, a designated successor trustee (often a trusted family member or professional) seamlessly steps in to manage the assets in your trust according to your wishes.

Drawbacks of a Living Trust

Cost and Time: Setting up a living trust can be more expensive and time-consuming compared to a simple will.

Funding the Trust: Assets must be formally transferred into the trust to be managed and distributed according to its terms.

Estate Taxes: While living trusts avoid probate, assets within the trust are still subject to estate taxes if your estate value exceeds the exemption limit.

Is a Living Trust Right for You?

Living trusts offer a clear advantage for those with significant assets to pass on. They streamline the inheritance process, maintain privacy, and offer greater control. However, for individuals with a modest estate, a basic will might be sufficient.

8 best US regulated forex brokers in 2024

Making the Right Choice

The best way to navigate this decision is to consult with an estate planning attorney. They can assess your unique situation, delve into your financial picture, and explain the pros and cons of both living trusts and wills. This personalized guidance ensures you choose the method that best suits your needs and protects your loved ones’ inheritance.

Remember, planning for the future is a gift to your family. By taking the time to explore your options, you can ensure your legacy is passed on smoothly and efficiently.

While living trusts offer significant advantages, they might not be the perfect fit for everyone. Here are some alternatives to consider:

Joint Ownership: Owning assets jointly with a beneficiary (like a spouse or child) allows them to automatically inherit the asset upon your passing. However, this approach offers limited control over the asset’s future use and can have unintended tax consequences.

Transfer-on-Death (TOD) Registration: This registration option allows you to designate a beneficiary for certain assets like bank accounts or investment accounts. Upon your death, the ownership automatically transfers to the beneficiary, bypassing probate. However, TOD registrations are limited to specific asset types.

Taking the Next Step:

Whether you choose a living trust, a will, or a combination of both, remember that estate planning is an ongoing process. Your circumstances and priorities can evolve over time. Regularly review your estate plan with your attorney to ensure it remains aligned with your wishes and reflects any changes in your life or financial situation. By taking a proactive approach, you can ensure peace of mind knowing your loved ones will be taken care of in the future.

Building Your Retirement Savings

Conclusion

While living trusts offer a streamlined and private inheritance process, they might not be suitable for everyone. Consider your specific needs and consult with an estate planning attorney to determine the best approach for securing your legacy and protecting your loved ones’ future. Remember, estate planning is an ongoing process, so revisit your plan regularly to ensure it remains aligned with your evolving circumstances.